share

Ready for Your Retirement?

Informed Decisions are one of Ireland’s only remaining independent financial advice firms. We specialise in retirement & investment planning for successful individuals, so that our clients only have to retire once.

Retire successfully with Informed Decisions.

informed decisions blog

Don't Be The Magpie, And Achieve Better Investment Returns

September 29, 2025

What is the investment “behaviour gap”?

The behaviour gap is the difference between the returns that funds deliver and the lower returns investors actually achieve. Morningstar’s Mind the Gap 2025 shows investors earned about 1.2% less per year than the funds themselves, mainly due to poor timing, panic selling, and chasing hot trends.

Don't Be The Magpie, And Achieve Better Investment Returns

Despite funds themselves delivering solid returns, investors on average capture significantly less. They say we got around 1.2% less per year over the past decade, than the investments actually deliver!

That mightn’t sound like a lot, but compounded over ten years, it equates to losing about 15% of your potential gains in a 10 year window.

So what’s going wrong? More importantly, how can you, as a thoughtful long-term investor, avoid falling into these traps, and give yourself the best chance of capturing your fair share of returns? Let’s take a look-see shall we.....

Oh, don't forget to register for our next public webinar, happening this Friday 3rd October with Alan Purcell from Cloud Accounts (Registration is complimentary here!).

The Return Gap: What It Means for You

Every year, Morningstar publish a fascinating study called Mind the Gap. The 2025 edition is just out, (access it here via a secure Tresorit Link I've created).

Once again it highlights one of the biggest challenges facing investors: we, the investing public, are often pretty daft!

Morningstar looked at more than 25,000 U.S. mutual funds and ETFs over the 10 years to the end of 2024. Here’s the key takeaway:

- Funds returned 8.2% per year (time-weighted) – what you’d have earned if you invested a lump sum at the start and held it untouched.

- Investors earned 7.0% per year (dollar-weighted) – what people actually earned when you factor in real-life buying and selling decisions.

That 1.2% shortfall is the “behaviour gap”.

It arises from mistimed buying and selling, chasing hot funds, panicking in downturns, or simply tinkering too much.

And here’s the sting: even good habits like drip-feeding investments can contribute to this gap, because they mean money isn’t invested for the full period. But it’s the bad habits such as panic sells and the FOMO buys, that really do the damage.

%20(1).png)

Who Struggled Most?

The study digs deeper into where investors capture more (or less) of their funds’ returns.

- Allocation funds (like target-date funds) had the narrowest gap – investors captured nearly all of the returns. Why? Because these funds automate diversification and rebalancing, so investors didn’t need to or weren't able to mess with the investment!

- Sector equity funds had the widest gap. Investors missed out on 1.5% per year here. These funds are often used speculatively, chasing tech or energy booms. It's kinda like 'Thematic Investing' which I see some firms advertise here. This is basically chasing the current hot topic (AI/Data centre currently, or ESG a couple years ago).

- Bond funds were another weak spot where investors captured only about half of the returns. Timing interest rate moves is notoriously difficult, and many tried (and seemingly failed).

- ETFs delivered higher raw returns but had bigger gaps than traditional 'mutual funds'. Why? Because they’re typically fully liquid you can buy and sell each day, and some investors couldn’t resist making a bags of it by over-trading!

The pattern is clear: the more opportunities we have to “do something,” the more likely we are to sabotage ourselves.

It reminds me of that wise investing mantra; 'Don't just do something, sit there'!

Why do investors underperform their own funds?

Most investors underperform because of emotional decisions — buying when markets rise, selling when they fall, or tinkering too much. Over-trading, chasing shiny new funds, or panicking in downturns reduces long-term returns compared to simply staying invested.

Why Does This Happen?

At its core, the return gap is about human behaviour.

We are wired to act. We want to flee when markets fall and to chase shiny things when they rise.

It feels safer and better and right in the moment, but it’s costly over time.

Morningstar also found:

- Higher tracking error funds (those straying from the benchmark) had bigger gaps. Investors struggled to stick with them.

- Funds with volatile cash flows (lots of people piling in and out) had worse results. More trading = less return.

- Cheaper funds had smaller gaps than expensive ones, but it wasn’t just about cost. The key was context: low-cost funds are often core holdings in advised investment and retirement accounts, where investors have an advisor between them and their trades, and so were more inclined to leave them alone, and do well as a result!

- Volatile funds had the biggest gaps. When funds swing wildly, investors are more tempted to jump in and out of the ship at the wrong times.

So yes, markets matter, fees matter and fund choice matters, but our behaviour as investors matters more.

The Consumer Outcomes

What does all this mean for you, sitting at your kitchen table, thinking about your pension or investment plan?

It means that success doesn’t just come from picking the “best” fund. It comes from creating a system and mindset that help you capture as much of the return as possible.

If your fund earns 8% but you only pocket 7%, that’s not a market problem – that’s a behaviour problem. And the solution isn’t more information, or more trading. It’s less.

How to Close Your Own Gap

Here are five practical steps to help you hold onto more of your investment returns over the coming decade (whatever they may be!):

1. Automate Everything You Can

The study shows investors in automated, all-in-one funds captured more returns. Why? Because they didn’t interfere. Use automation for contributions, rebalancing, and even withdrawals in retirement. Less temptation, less tinkering. Ideally, have an advisor who will stop you making a bags of things should you feel the urge!

2. Low-Cost Core Holdings

While cheap funds aren’t a silver bullet, they tend to be used in more disciplined ways. Build your portfolio around globally diversified, low-cost funds or ETFs that you can hold for decades (assuming this meets your volatility, returns, risk profile etc).

3. Beware of 'Exciting' Funds

I was quoted in the Sunday Times at the weekend re unregulated investment funds - where I continue to beat the drum for transparency and consumer protections around these things. Specialist funds like tech, biotech, or energy can look tempting, but they’re also where the biggest gaps (and capital risks) often appear. If you must dabble, keep it tiny and treat it as fun money, not core money.

4. Reduce 'Trading' to a Minimum

The data is unambiguous: the more you trade, the less you earn. Before making any change, ask yourself: 'Am I reacting to headlines, fear, or FOMO? Or is this genuinely part of my long-term plan?' If it’s the former, resist, and sleep on it.

5. Build a Margin of Safety

Morningstar suggests “haircutting” your expected returns to account for inevitable gaps. For example, if your financial plan assumes 6% growth, maybe plan for achieving 5%. That way, even if behaviour costs creep in, your plan remains intact?

The Role of a Financial Plan

A solid financial plan and an advisor should ideally be your anchor. It sets out your long, short and medium term goals, clarifies the role of each investment pot (as I call them), and helps you easily stay the course when markets test your nerves or tempt you with shiny things. Don't be the magpie!

At Informed Decisions, we often remind clients: the market will do what it does, but your job is to control what you can – costs, discipline, behaviour. The rest is noise.

That’s why financial planning isn’t just about numbers. It’s about emotion, perspective, and thinking about your future selves.

When you know your plan is robust, you’re less tempted to make rash decisions. You are less tempted to be the magpie.

Plus, you'd hope that your financial planner and advisor would have helped you stay not simply invested, but invested in productive vehicles and staregies.

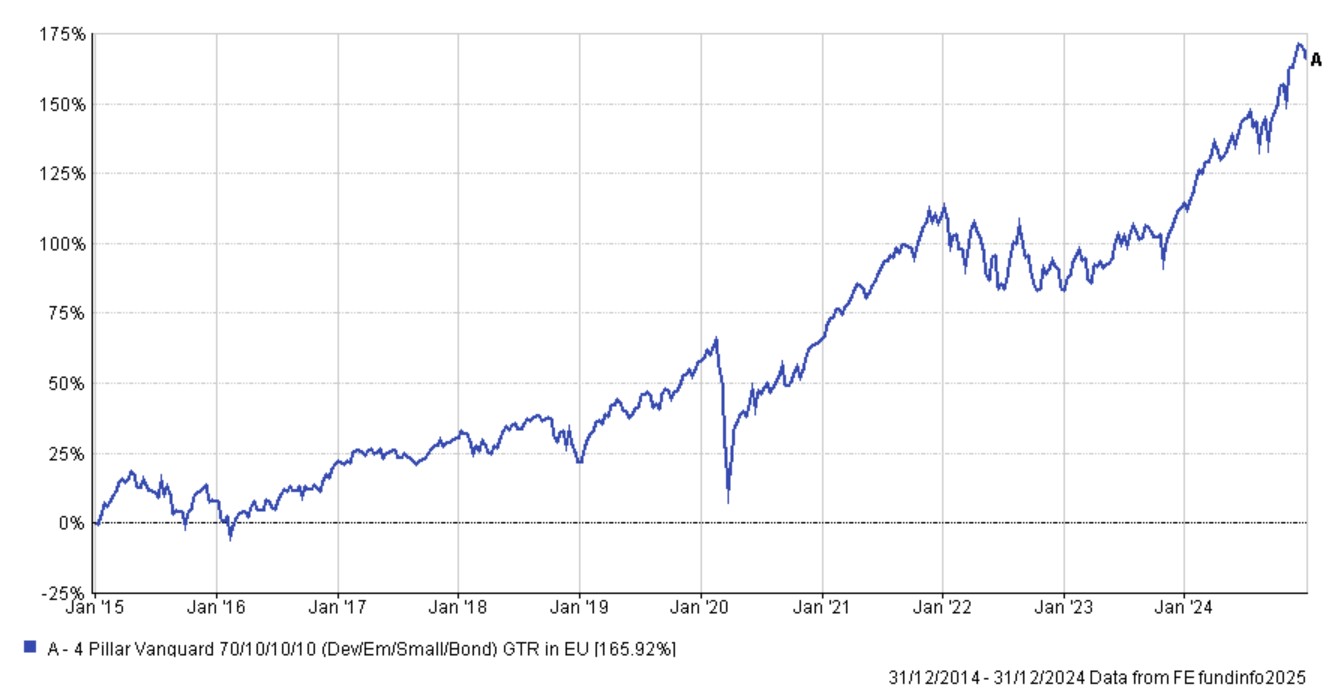

Here's a sample Vanguard 90% Equity and 10% Bond portfolio we've deployed for some, which delivered 165% gross in the same 10 years, or over 10% annual returns.

Final Thoughts

The Mind the Gap 2025 study is sobering, but it’s also a great reminder (hence me sharing it!?).

It reminds us that the biggest determinant of success isn’t whether the MSCI or S&P 500, or Eurostoxx 50, or whatever you are watching goes up or down next year, but whether you stick with your strategy through thick and thin.

The good news? The gap isn’t inevitable.

With the right structures, mindset, and support, you can tilt the odds firmly in your favour.

So, if you take just one thing away from this piece, please let it be this:

Investment success is less about picking winners and more about avoiding unforced errors. (much like the game of tennis!).

Do less. Stay the course. Capture more of what the market is giving you.

That’s how ordinary investors achieve extraordinary outcomes.

The financial media is whipping us into a frenzy, so when the next slap in the chops comes along - maybe read this aloud each night before bed!

I hope it helps.

Thanks,

Paddy.

Disclaimer

The content of this site including blogs and podcasts is for information purposes only. Everybody’s financial situation is different and the content we share on our site and through podcasts may not be applicable to you.

The articles, blogs and podcasts are not investment advice. They do not take account of your individual circumstances, including your knowledge and experience and attitude to risk. Informed Decisions can’t be held responsible for the consequences if you pursue a course of action based on the information we share

How can I avoid losing returns to bad behaviour?

You can reduce the behaviour gap by automating contributions and rebalancing, focusing on low-cost diversified funds, limiting trading, and having an advisor or plan to keep you disciplined. The key is to stay invested and avoid reacting to short-term noise.

You may also like...

June 8, 2026

Bonds in Retirement Ireland: Are They Still Worth Holding in Your ARF in 2026?

find out more

.jpg)

Retired or close to it?

Informed Decisions are one of Ireland’s only remaining independent financial advice firms. We specialise in retirement & investment planning for successful individuals, so that our clients only have to retire once.

Find out how we can help...

.svg)