share

Ready for Your Retirement?

Informed Decisions are one of Ireland’s only remaining independent financial advice firms. We specialise in retirement & investment planning for successful individuals, so that our clients only have to retire once.

Retire successfully with Informed Decisions.

informed decisions blog

Your Essential Pre-Retirement Checklist!

December 15, 2025

Should I change my investment portfolio before retirement?

Some adjustment often makes sense, but sweeping moves to cash rarely do. Aim for a blend of growth assets and a cash buffer.

Your Essential Pre-Retirement Checklist

Retirement starts long before you hand back the laptop or walk out of the office for the last time!

The real work happens in the final decade, when you bring everything together; pensions, savings, tax, debts, lifestyle, and the practical bits that make life run smoothly.

This pre-retirement checklist Ireland will hopefully give you a clear, practical path that helps you can step into the next stage with clarity and confidence (not a big ask is it!?).

What we'll explore in this piece:

• How to calculate your retirement number

• How to review pensions and income sources in an Irish context

• How to tidy up investments without derailing long-term returns or compounding

• The key tax and admin tasks to complete before leaving work

• When professional planning adds value

Know Your Retirement Number

Most people worry about retirement because they’ve never really sat down to calculate the one thing that matters:

How much income do you need each year to live the life you want?

My advice is to do this yourself, and indeed seek a professional to help you. You'll be that bit more informed and planned if you do some homework yourself first.

Here are a few steps....

Estimate your annual spending

Start with your current spending.

Pull a year of bank records (most allow excel 'export'). Add irregular items such as:

• Home repairs

• Holidays

• Car replacements

• Medical bills

• Family support/gifting

Aim for a realistic number on what it costs you to live and do the stuff you like to do. Try not to play it down, that'll hurt you in the planning phase! If you spend €70,000 per year today, that’s a better guide than trying to squeeze it into €50,000 later!

Consider mortgage status

If your mortgage will be cleared before or around retirement, great. That lowers your required income, or gives you more 'fun money' potentially.

Factor in Irish tax bands

Your gross income requirement depends on which band your income falls into. For example, a retired couple drawing €70,000 may have very different net outcomes depending on how the income is split between them. Check out the recent piece we did on income tax planning when drawing pension incomes.

Calculate the income gap

Work out:

Annual spending minus secured retirement incomes = what your pensions and investments must provide.

This is the heart of every retirement plan.

Assess Your Retirement Income Sources

Once you know the target, add up all potential income streams.

The State Pension

The State Pension (Contributory) currently pays up to €277.30 per week, if you meet the full contribution requirements.

It starts at 66, though this may change in future.

Check your contribution record on MyWelfare.ie so you know whether you’re on track for a full or pro-rata pension.

They actively discourage it but if you get talking to the guys over the phone there, they are usually great support and assistance.

Occupational pensions

Many Irish professionals have defined contribution schemes through work.

Take a little time to review:

• Current value

• Investment mix and allocations

• Charges

• Employer contributions

• Your own contributions and AVCs

When it comes time to draw-down, you will convert these Defined Contribution schemes into tax-free lump sums (optional), plus annual income via an Approved Retirement Fund (ARF) or Annuity.

PRSA's and Personal Pensions

These sit outside employer schemes but are essentially the same thing - assets for future enjoyment!

And given the Auto Enrollment drive that is going on at the minute, it seems every employee in the country earning over €20,000 per year, will either be a member of MY Future Fund or have a PRSA! And that's a positive in regards overall pension coverage. All of these of course count just the same for retirement funding.

Rental income

We're not going to argue the pros and cons of being a landlord here and now (please read this piece by me if you want to dig deeper?).

But rental income can certainly be a diversified and positive income for the owner.

However, it is not a panacea;

• It’s taxable income, even if and when you don't need the income (much like dividend stocks!)

• It requires management

• It’s not always stable or stress-free, but when it works it can work really well!

Landlords are reportedly selling-up at record levels, but there will always be those who remain. I often think that when 'the masses' are leaving something, it's usually a sign that there'll be benefit staying (apart from when it's a literal burning building!).

So include realistic, not optimistic, figures in your calculations here.

Are you on track?

A simple rule of thumb is that drawing 3–4 percent of your total pension and investment pot each year is broadly sustainable for many long retirements.

But the rule breaks down if you retire really early (in your 40's!), withdraw sharply in down markets, or hold too much in extremely low-volatility assets, or high-volatility assets without a buffer.

Review and Optimise Your Investments

In the final decade, many people are encouraged to 'lifestyle' and shift everything into defensive assets or cash.

That often causes more harm than good.

You may have caught our 'Risk of Ruin' piece from April 2024 which shared deep research about the long-term outcomes of both defensive and aggressively allocated portfolios over many retirement scenarios. The results might surprise you.

Keep growth working for you

Retirement will last four decades for some. You still need growth to protect yourself from the erosive powers of inflation.

Consider a balanced approach

For many Irish retirees, holding somewhere between 60–80% global equities, depending on risk tolerance and ability to bear loss, keeps long-term returns on-track. And yes, there will be times when they'll question that decision, but over the long-term, history has shown this to be a very prudent thing to do for most.

Build a buffer

A common approach is to hold 2–8 years of spending in lower-volatility assets across portfolios. Depending on the structure, these may be short-dated bonds, money market funds, cash or deposits. This can often help protect us from selling equities during a temporary market decline, of which we will experience many in a 4 decade retirement!

Tidy Up Your Pension and Investment Admin

This is the boring but important part of a pre-retirement checklist Ireland plan.

Beneficiary nominations

Ensure all pensions and investment accounts have up-to-date beneficiary details. Many people forget this after job changes.

Consolidation

If you have older pensions from previous employers, consider whether it makes sense to bring them together.

Benefits include:

• Lower fees

• Easier management

• Clear and aligned investment strategy

But only after comparing charges and features as sometimes it will make sense to laev them as they are and/or wait for exit penalties to expire etc.

Check ownership structures

Joint accounts, single-name portfolios, ARFs, and property ownership all affect tax in Ireland.

Tidy them up now, before retirement income begins. Speak to accountant and tax advisor to ensure all is as it should be

Review charges

Small percentages compound over decades. Review investment and pension fees to ensure you’re getting value.

Reduce or Clear High-Cost Debt

Debt isn’t always a problem, but high-cost debt such as car loans and credit cards heading into retirement can create cashflow issues, needless costs and potential stress!

Prioritise

• Credit cards

• Personal loans

• Car finance

• Large mortgage balances approaching retirement

Clearing these improves your cash flow and brings huge peace of mind.

Many often think and feel that they'll get more financial gain by investing instead of clearing debt. They may or they may not- but if they clear the debt they are guaranteeing the debt and monthly repayment is gone!

Tax Planning Before Retirement

Ireland offers generous pension tax relief. The final working years are often the best time to use it.

Maximise pension contributions

You can receive tax relief up to age-based limits, capped at €115,000 of income.

If you are 50 to 54 years of age, you are entitled to put 30% of earnings into pension and get full tax relief.

If you are earning €115k or more, that is €34,500 per year, on which you can get 40% (€13,800) tax relief on.

Aged 55 to 59, it's 35% of €115k you can contribute.

For many professionals in their 50s, this is where large AVCs combined with employer-pension top-ups can be extremely valuable and fruitful.

Timing matters

A contribution made before the tax deadline might save you thousands in income tax and/or wipe out a potential tax bill.

Prepare for drawdown taxation

• Pension lump sums can offer up to €200,000 max tax-free cash.

• ARF withdrawals and Annuity payments are taxed as income.

• USC and PRSI may apply depending on age and income type.

• Pension splitting between partners can optimise tax bands.

Build a Retirement Income Plan

This step connects everything.

It answers the real question: How will you actually pay yourself when the pay cheques stop?

Early retirement years (50–65)

You may rely more heavily on pensions, investments, rental and savings before the State Pension kicks in.

Middle retirement (65-75)

Often more stable, with consistent drawdowns from ARFs, State Pension and/or investments.

Later retirement (75+)

Spending sometimes reduces, but healthcare or home-help costs might increase.

Avoid forced sales

A cash/income buffer allows you to avoid selling large portions of your equities in a market decline, which can be of the most damaging actions a retiree can make.

Protect your partner

Ensure surviving-spouse income is secure.

Plan pension beneficiary options and the flow of income if one partner dies early.

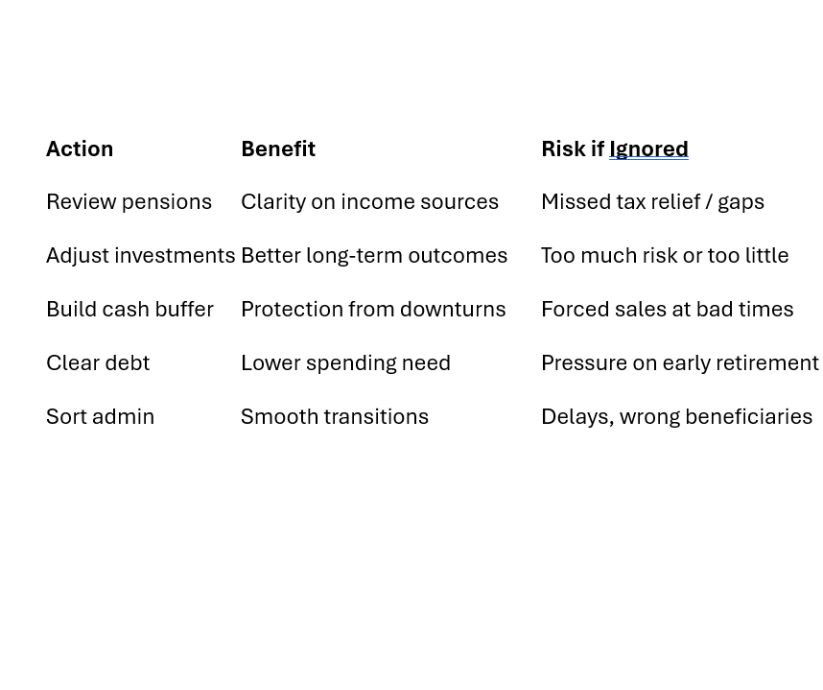

Comparison Table: Key Actions vs Outcomes

How do I know if my pension is enough?

Work out your spending, subtract guaranteed income, and see whether your pensions and investments can support the gap at a sustainable withdrawal rate.

Organise the Practical Side

It’s not all about money.

These steps protect both you and your family.

Wills and Enduring Power of Attorney

Ensure both are updated and valid.

If you don't have both - now is the time to act!

Key documents

Gather everything into one secure folder, digital or physical, which is accessible by all that need it!

• Pension statements

• Investment accounts

• Property documents

• Insurance policies

• Bank details

• Relevant passwords (stored securely)

Insurance review

Life covers, mortgage protection policies, and income protections should all be considered before retirement—not after.

When to Work with a Planner

A professional adviser can:

• Stress-test your retirement number

• Optimise tax planning for couples

• Review investment strategy and align with your plan and timings

• Build an income plan to optimise assets and incomes into the future, and on an on-going basis

• Help you stay invested 'properly' and avoid investment mistakes during market swings

For many, the final decade before retirement is the period that benefits most from expert guidance, preparation and planning.

Don't leave it too late!

And I wish you the very best of good luck with it all.

Paddy Delaney QFA RPA APA

Disclaimer

The content of this site including blogs and podcasts is for information purposes only. Everybody’s financial situation is different and the content we share on our site and through podcasts may not be applicable to you.

The articles, blogs and podcasts are not investment advice. They do not take account of your individual circumstances, including your knowledge and experience and attitude to risk. Informed Decisions can’t be held responsible for the consequences if you pursue a course of action based on the information we share

How much cash should I hold before finishing work?

Many Irish retirees hold 2–8 years of expected withdrawals in low-volatility assets.

You may also like...

August 3, 2026

Zombie Funds: What Nobody Tells You About Private Credit and Equity in Ireland

find out more

Retired or close to it?

Informed Decisions are one of Ireland’s only remaining independent financial advice firms. We specialise in retirement & investment planning for successful individuals, so that our clients only have to retire once.

Find out how we can help...

.svg)