share

Ready for Your Retirement?

Informed Decisions are one of Ireland’s only remaining independent financial advice firms. We specialise in retirement & investment planning for successful individuals, so that our clients only have to retire once.

Retire successfully with Informed Decisions.

informed decisions blog

Markets Are High...Should I Jump To Cash, Out Of Equities?

November 24, 2025

What if a crash is obviously coming?

It rarely is when we think it is! Every major crash in modern history was 'predicted' by hundreds of analysts, most of whom predicted dozens of crashes that never arrived. Evidence shows prediction success is almost always random.

Is now the right time to move a chunk of your investment or pension assets out of equities, and into Bonds, Money Market Funds or Cash?

It's a question that you may be asking because of a headline you read, an online commentator with a scary statistic, or someone you chatted with spoke of impending doom!

I'll not tell you here whether you should or you should not, but I will briefly share actual potential outcomes for you to consider, before you give it another seconds' thought!

Markets Are High: Should You Sell Your Equities Now?

When markets are high, it’s natural to wonder 'should I sell equities when markets are high and lock in gains?'

At first glance it seems like the right thing to do in all eventualities, particularly if you've 'done well' in recent decade etc.

If you’re in your 50s, earning well, and considering retirement, the question feels even sharper.

This piece gives you a clear, evidence-based view of what usually happens after market highs, what Irish investors actually risk by bailing out, and how to check if a change in risk makes sense for your plan.

You’ll learn:

• What markets tend to do after hitting new highs, and what's the worst that could happen!

• Why selling out can backfire for Irish investors

• How to handle risk if retirement is close

• What a practical plan looks like in real life

• Questions to ask yourself before changing anything

Why 'Markets Are High' Feels So Uncomfortable

While it might be comforting to see your savings and pension assets values higher than they have been before, it's a double-edged feeling!

If you lived through 2000, 2008 or 2020, market highs can feel like standing on the edge of a cliff, you're just waiting for the fall!

Some of us get vertigo, naturally. You’ve seen how fast things can reverse.

Two common worries show up:

• Fear of a crash wiping out hard-earned savings and retirement assets that you intend to use and then bequeath!

• Worry that retiring soon means you 'won’t recover' if markets fall

When headlines talk about peaks, corrections or bubbles, it’s easy to think other investors know something you don’t, that the 'smart people' have bailed, so you should too! That feeling alone can push people to jump to cash.

The truth: markets hit highs far more often than we might think.

Global equities have spent roughly 30 percent of trading days at or near all-time highs over the past 40 years.

Yes, almost 1 in 3 trading days has been an all-time high in the past 40 years.

High doesn’t mean due for a fall.

It just means prices reflect the latest earnings, growth, and expectations for the future earnings of the great companies of the world.

Granted, there hasn't always been such drama, controversy and speculation about the future, as there is today, but it hasn't been smooth sailing either!

And it is when things do go wrong, which they do regularly, that we see the real impacts.

And the only reason anyone would jump to cash is to try protect their savings or pension assets from a bear market.

What Actually Happens During and After Bear Markets

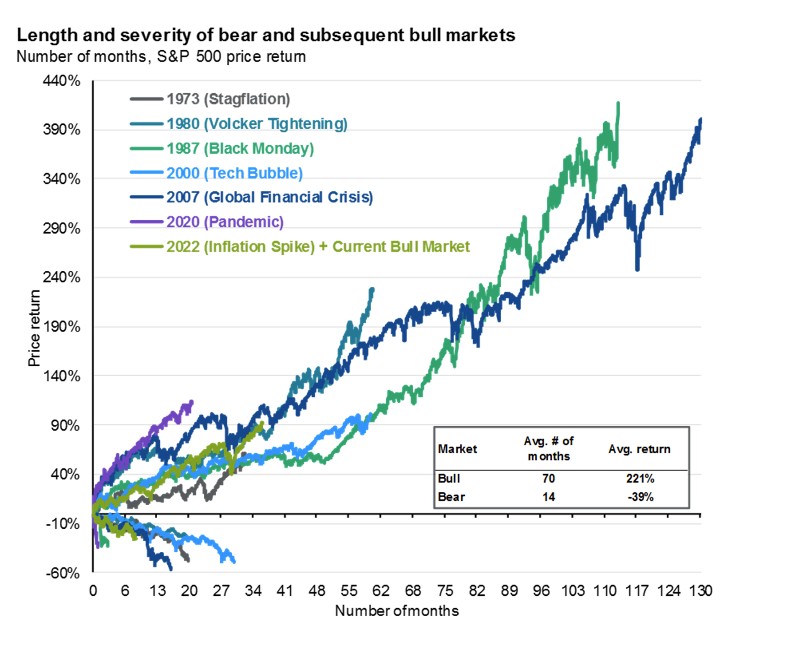

The below graph from J.P Morgan Guide To The Markets says a lot.

It is specific to the S&P 500 and covers everything from the 1970's stagflation to recent times.

The average Bear (Negative) Market lasted 14 months (Longest was tech Bubble at c30 months) and returns average -39% total

The average Bull (Positive) Market lasted 70 months (Longest we're in is now, following the GFC, and returns average +221%

The upside is better than the downside.

What About After All-Time Highs?

Looking at major global indices since the 1970s, the average 1-year return after an all-time high is positive.

Not guaranteed, not steady, but positive more often than not.

That’s because markets usually reach highs during expansion, not mania.

Ireland and Europe follow similar patterns

European and Irish pension funds, including the large diversified funds used in PRSAs and occupational schemes, show the same pattern.

After many of their own peaks (2013, 2017, 2021), the following 12–36 months delivered mixed but normal returns. Not system-wide collapses.

Headlines make it feel worse than it is

News edits out the boring middle ground.

You’ll hear extremes:

• 'This Time It Is Different.....Crash Incoming'

• 'Another All-Time High As Markets Peak'

• 'Tech bubble 2.0'

Quiet years rarely make the front page.

I rather enjoyed coming-up with those titles, think I should get into the tabloid business!

What's The Worst That Could Happen?

If history did repeat, and markets fell by c50%, and didn't recover for years, what could that look like?

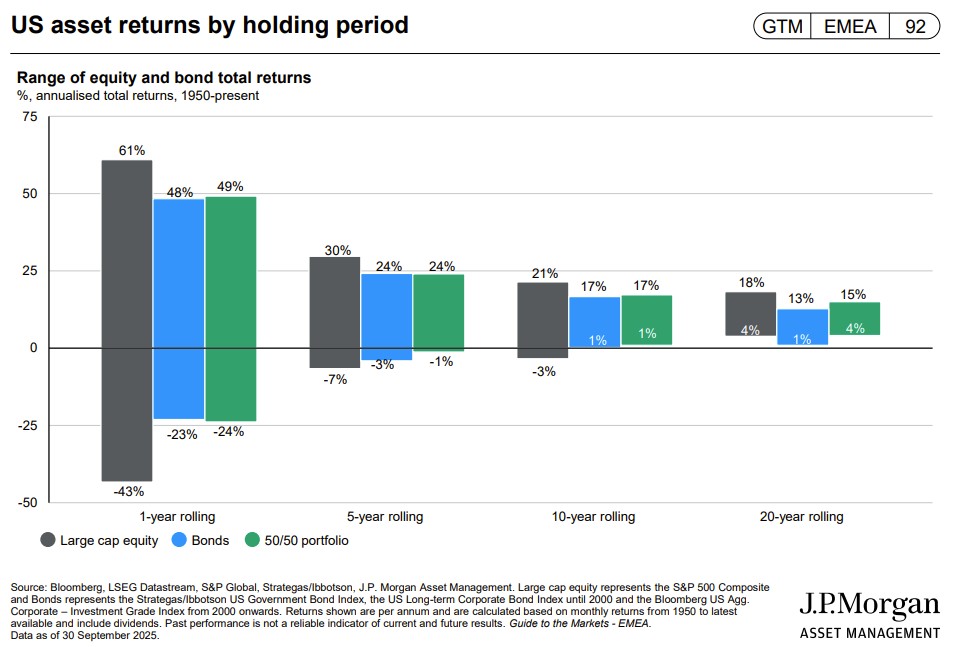

Well thanks again to J.P Morgan Guide The The Markets (US), here's one we prepared earlier!

Holding S&P500 equity only, between 1950 and Q4 2025:

Worst 1-year returns were -43% (ouch)

Worst 5 year returns were -7% (fairly ouch)

Worst 10 year returns were -3%

Worst 20 year returns were +4%

Seeing as the point I'm exploring here is the worst we've experienced we don't need to dwell on the fact that S&P500 tends to go more south than rest of the wolrd when things are going south, not the fact that best 1 year was +61%, 5 year 30%, 10 year 21% or 20 year 18% annually. We don't need to labour that point, OK, we don't!

The Real Risks: Selling Out & Getting Back In

Market-timing is usually more damaging than the downturn that we fear.

Three issues hurt investors the most:

Missing strong days

If you bailed to cash, you might possibly somehow miss a generational market decline. Slim but possible.

However, you will likely also miss the recovery days. And missing the best 20 days of the MSCI World over the last 20 years, your return was roughly half of staying invested through the bad and the good.

The best days often cluster around the worst days.

Bail out before or during a dip… and you usually miss the rebound.

Locking yourself into cash

Cash is stable, but inflation is not.

At Ireland’s 4–6% inflation levels in recent years, €500,000 in cash can lose €20,000+ of real spending power in a year.

I've seen people move to cash way before declines, so they miss the say 20% growth before the next decline. Plus, they are paralysed to get back into markets during or after that decline. Possibly forever. And you don't recover from that.

Creating self-made losses

Many investors sell after a shaky period, not before it. They then buy back only when markets 'feel safe' again, which is usually at a higher price!

This is a sure-fire recipe for disaster for you and your savings/pension assets.

What's Next For Global Equities?

We don't know. Now that that is out of the way.....

Vanguard shared a 'forecast' in January of this year titled 'What Next For Equities After A Decade of US Outperformance' and you can access it here. It's for professional investors, so read with caution!

Interestingly, they suggested the next 10 years may look like the following:

'Compared with last year’s Vanguard economic and market outlook, we expect slightly lower returns for US equities, with a median 10-year annualised forecast of 3.9%, while our outlook for UK equities has improved, to around 6.7%. For global ex-UK and global equities—which contain a large allocation to the US—we expect returns of around 5.2% and 5.3%, respectively. For developed market ex-US equities, we expect returns to be around 8.4%, reflecting the more attractive valuations outside the US market that we expect to matter in the long term.'

We'll see if they were right or not - so far they are way-off (YTD S&P500: 12.5%, Emerging Markets c13%!)

Should I move to cash temporarily?

Short breaks in cash often turn into long waits. If you need less risk, adjust strategically rather than timing in and out.

If You're Near Retirement, What Should You Do?

Being in your 50s means you’re getting closer to drawing from pensions, ARFs or investments.

That doesn’t automatically mean selling out of equities, as you may have seen in our piece about LifeStyle Funds??

It does mean assessing sequence-of-returns risk.

What is sequence risk?

If your portfolio falls sharply while you’re obligated to be withdrawing income, the damage can compound faster.

A 20 percent drop in a €1m fund when you’re taking €40,000 a year hits harder than the same drop when you are 45 years of age and accumulating, particularly if it sticks-around for years.

This is where a structured approach helps:

Consider a cash or 'income reservoir'

Many retiring clients hold roughly 2–8 years of withdrawals in low-volatility assets within their ARF.

This gives markets breathing room without ditching equities entirely.

Adjust, don’t abandon

Moving from say 90 percent global equities to say 70 percent global equities is a genuine reduction in volatility and something that some decide to do, for their own peace of mind (as opposed to their financial security). However, going to 0% is usually a reaction to fear, not a plan.

Blend your pension pieces

Most Irish retirees mix:

• ARF (flexibility and growth)

• Tax-free lump sum and savings on deposits

• Some guaranteed income from rental, old Defined Benefit schemes, State Pensions etc

A Simple Irish Example

Imagine a 55-year-old executive in Carlow with:

• €1,400,000 combined pensions

• €250,000 in personal savings/deposits

• Planning/Hoping to retire at 58

Two paths:

Path A: Sell everything at a high

Move all pension funds to cash or very low risk.

Inflation at say 3% erodes about €150,000 of real value over 3 years.

Re-entry, if choosing ARF, will almost certainly happen when markets 'feel calmer', i.e. historically at higher levels.

Path B: Stay invested with a buffer

Keep say 70-90% percent in global equities, with balance in defensive assets for defensive reservoir.

Short-term swings remain, but long-term growth typically outpaces inflation.

The retirement plan stays on track unless markets behave far outside historical norms - in which case plan could still sustain them depending on withdrawal rate and income need.

Conclusion: An Evidence-Based Approach

Smart practices and common-sense to follow over the long-term, for most of us;

• Set a policy rather than reacting to headlines

• Use rebalancing rules to control risk, and across entire holdings

• Keep at least a decent allocation to diversified equities for long-term inflation protection

• Treat 'market highs' as insignificant information, not a signal or rationale for re-allocating your assets!

Your plan, not the news, nor the crystal-ballers should decide your risk level.

I hope this helps.

Paddy Delaney QFA RPA APA

Disclaimer

The content of this site including blogs and podcasts is for information purposes only. Everybody’s financial situation is different and the content we share on our site and through podcasts may not be applicable to you.

The articles, blogs and podcasts are not investment advice. They do not take account of your individual circumstances, including your knowledge and experience and attitude to risk. Informed Decisions can’t be held responsible for the consequences if you pursue a course of action based on the information we share

Is it a bad time to retire when markets are high?

Never a bad time to retire! It depends on your mix of guaranteed income, defensive asset 'reservoirs', cash buffer, and type of fund/equity being used.

You may also like...

July 6, 2026

Sequence of Returns Risk in Ireland: Why the First Decade of Retirement Decides Everything

find out more

June 22, 2026

Reducing Investment Risk Before Retirement: What Most Irish Pension Holders Get Wrong

find out moreRetired or close to it?

Informed Decisions are one of Ireland’s only remaining independent financial advice firms. We specialise in retirement & investment planning for successful individuals, so that our clients only have to retire once.

Find out how we can help...

.svg)