share

Ready for Your Retirement?

Informed Decisions are one of Ireland’s only remaining independent financial advice firms. We specialise in retirement & investment planning for successful individuals, so that our clients only have to retire once.

Retire successfully with Informed Decisions.

informed decisions blog

The Financial Freedom of Getting Kids Off The Books!

November 17, 2025

How much do Irish parents spend on adult children?

Many spend between 10000 and 20000 a year depending on rent, transport and general support.

The Financial Freedom of Getting Kids Off The Books

If you have kids, of any age, you'll know that they cost money, real money!

You spend years helping your kids find their way. Then one day you realise they are grown adults and still leaning on your bank account!

This piece gives you the facts and the numbers that often surprise people in their fifties.

You will learn:

• How each adult kids can add c€15k-€20k per year of additional cost to your household

• how that support shapes your retirement choices

• ways to help them stand on their own feet

• simple Irish tax points that matter

Why This Matters For People In Their Fifties

Your fifties are usually the years when financial pressure eases. The mortgage may be calmer, income is steadier, and kids are mostly launched. Then rent rises, college lasts longer than expected, or an adult child returns home.

You want to support them. You also want to protect your retirement timeline. When those interests clash, your savings usually take the hit. Even two or three years of reduced saving can delay retirement more than most people expect.

What Keeping Kids On The Books Really Costs

Typical support areas

Many of the people we support have adult kids who are still 'on the books'. From our experience, parents in Ireland regularly cover:

• Rent & college costs

• Car insurance & use of a small car

• Health insurance

• Hefty food & entertainment expenses!

Irish examples

A simple breakdown many households will recognise:

• Rent support: 500-800/month

• Car insurance: 200/month

• Health cover: 100/month

• Food/entertainment/general: 300/month

That amounts to €1,100-€1,400 per month.

Over a year it is €17,000, of net income to cover the potential costs of an adult child!

If we total that for 4 years, we're talking about €60,000-€70,000 of income or capital required per big child!

That money either supports your kids or supports your own freedom.

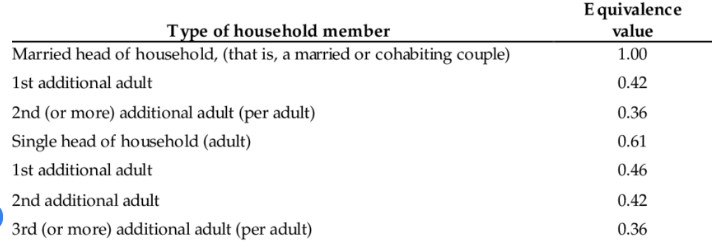

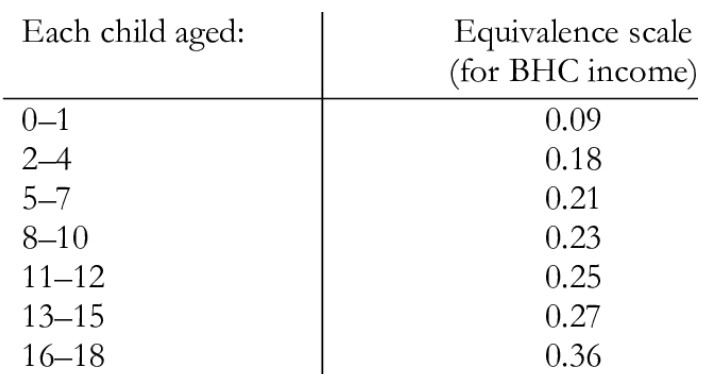

The McClements Equivalence Scale

The McClements Scale, from UK research but fully applicable to Ireland, helps us understand how household costs rise and fall as kids grow-up, join or leave the home.

It converts everyone into “equivalent adults” and shows the true financial weight each person brings.

To convert this to practical numbers, take a scenario:

Jane & Jack's Household Costs Over Time

Jane's (head of household) total costs are €50k per year

She gets married to Jack, who brings much fun ;) but also an additional factor of 0.42, or €21k

The total to run their household is now €71k.

They then have 2 kids, for this example.

While they are under 18, each child will vary in additional costs from a factor of 0.09 to 0.36 (or from €3,600 per year when a baby, to €14,400 when they are 16 to 18!!).

Jane and Jack notice that as the 2 kids get older, their household expenses climb up steadily!

When it was just the 2 of them, their total household cost was €71k.

That increases by a factor of 0.27 (of €50k) per child when the kids are 13-15, for a total of c€92k per year, or €7,700 per month.

As they pass into adult-hood and are STILL on the books, McClements suggests that the additional financial burden on the household is

0.42 for the first child (c€21k per year for Jane & Jack) and 0.36 for the 2nd child, or €18k per year.

While they are adults and on the books, McClements suggests 'these 2' will cost c€40k per year!

I hope they appreciate you!

The McClements Scale makes one thing clear: when an adult child moves out, your long-term financial capacity increases immediately and meaningfully.

How Adult-Child Support Delays Retirement For Some

Impact on pension contributions

Cashflow pressure often leads parents to reduce pension contributions for a year or two. Even short pauses can reduce your long-term fund noticeably.

Instead of sending €30k a year to support, educate or enable their 2 children to grow, imagine Jane and Jack directing that into their pension and claiming the higher-rate relief! Net cost might fall to about €18k per year, and accumulate c€150k in 4 years.

Over time that difference can add a decent six-figure value to their retirement plans!

Reduced savings

Monthly support for kids often replaces monthly saving. The more support you give, the slower your own plan moves for many.

A simple example

One client supported two adult children during late-stage college at a cost of roughly 12,000 a year. When both kids started working, they set a clear finish date for support. Redirecting that money to pensions, to maximise tax reliefs, and cash reserves changed their financial picture within two years. They regained control and moved closer to real choice about work and retirement.

When It Is Reasonable To Step Back

What other Irish parents do

Most Irish parents expect or hope to provide some help until their kids reach full-time employment. After that, an agreed finish date is common. It avoids confusion and resentment on both sides. Setting clear expectations and timelines is a valuable endeavour. Having said that, everyone's situation will be different of course, and some will be ready before others etc.

A transitional plan

• agree a finish date

• step down support gradually

• help them build a simple budget

• stop covering surprise bills - let them figure it out!

• encourage them to take responsibility and awareness early

Can financial support reduce my pension tax relief?

Yes. If support reduces your spare income, you may contribute less and lose valuable reliefs, potentially.

Helping Kids Become Financially Independent

Starter budgets

Encourage your kids to structure their own spending. Key items include:

• rent

• food

• transport

• savings

• fun money

Most people in their twenties drift into spending habits. A simple plan helps them find stability and restraint, maybe!

Simple Irish tax points

Parents can give up to 3000 per child each year under the small gift exemption without affecting the child’s lifetime threshold for gift or inheritance tax. If you want to provide larger help, keep thresholds in mind.

Protecting Your Own Long-Term Security

Are you compromising your retirement

Support for kids feels generous, and for any parent, it is something they will at least consider! But it often reduces your pension funding or slows your investment plan. You can give money later. You cannot reclaim the lost years of compound growth.

Your own freedom number

Your own financial 'number' is the annual income you want and the lump sum needed to support it. Once you know that figure, you can judge how long you need to work and how much you can afford to help.

The cashflow turning point

Once kids leave the books, monthly cashflow often improves by c15-20% of joint-household total costs!

The McClements Scale backs this up, showing that removing one adult reduces real household costs in a meaningful way.

Conclusion

Most of us want to be in a position of financial independence when kids leave home. We might get that freedom based on our own accumulated assets, or that plus a combination of getting kids off the books! When support for kids tapers off and your own pension and savings rise again.

A small shift in how you support can change your entire retirement timeline. Your next step is simple: check your own numbers and agree a finish date with your kids!?

If you want clarity on your own financial freedom and when you can choose a lower-pressure life, get in touch.

You can also read or listen to our award-winning blog and podcast for (hopefully) fresh thinking rooted in reality.

I hope this helps.

Paddy Delaney

Disclaimer

The content of this site including blogs and podcasts is for information purposes only. Everybody’s financial situation is different and the content we share on our site and through podcasts may not be applicable to you.

The articles, blogs and podcasts are not investment advice. They do not take account of your individual circumstances, including your knowledge and experience and attitude to risk. Informed Decisions can’t be held responsible for the consequences if you pursue a course of action based on the information we share

Can I retire while still helping kids?

Sometimes, yes. The only accurate answer comes from a cashflow plan based on your own numbers.

You may also like...

June 8, 2026

Bonds in Retirement Ireland: Are They Still Worth Holding in Your ARF in 2026?

find out more

May 18, 2026

Risk and Reward in Retirement: What Ben Carlson’s Research Means for Irish Investors

find out moreRetired or close to it?

Informed Decisions are one of Ireland’s only remaining independent financial advice firms. We specialise in retirement & investment planning for successful individuals, so that our clients only have to retire once.

Find out how we can help...

.svg)