share

Ready for Your Retirement?

Informed Decisions are one of Ireland’s only remaining independent financial advice firms. We specialise in retirement & investment planning for successful individuals, so that our clients only have to retire once.

Retire successfully with Informed Decisions.

informed decisions blog

The Silent Thief: What Inflation Is Doing to Your Cash Savings in Ireland

March 16, 2026

How much does inflation reduce the value of cash savings in Ireland over time?

At Ireland's long-run average inflation rate of around 2.5% per year, €100,000 in cash loses roughly 22% of its purchasing power after 10 years, 39% after 20 years, and over 50% after 30 years. The money still exists — it just buys significantly less.

There's a particular comfort in keeping large amounts of money in current and deposit accounts. It's there. It's solid. The number on the screen doesn't move when markets wobble. And after the inflation and market shocks over recent years, many Irish savers understandably let cash pile up.

But here's the thing nobody puts on a deposit account brochure: "Cash doesn't stay still". It just looks like it does!

Ireland's Cash Mountain

Before we get into the numbers, let's acknowledge the scale of what we're talking about.

Irish households currently hold a staggering €172 billion on deposit. Around 85% of it is earning next to nothing on over night accounts, demand deposits and the likes, earning zero interest. The banks love us for this; as they get to use those deposits to make money on our money!

To put that in context, nearly 90% of Irish household deposit balances are held in overnight or demand accounts; a much higher share than the euro-area average of around 55%.

Estimates suggest that if Irish deposits were earning interest at the euro-zone average rate, households would have earned €788million more in interest income in 2024 alone. That is a staggering collective opportunity cost. And it's entirely self-inflicted.

Why does this happen?

Irish investors still carry the memory of bad investing experiences; plummeting Eircom shares in 1999, collapsing bank shares after the 2008 financial crash etc etc. Those memories created a deep psychological attachment to the apparent safety of cash. Many Irish savers associate investing with volatility and potential loss, even though long-term, diversified investments have consistently outperformed cash over meaningful time horizons.

What Inflation Actually Does to €100,000 in Ireland

Now let's get to the real problem. Ireland's average annual CPI inflation over recent decades has been roughly 2–2.5%, though it peaked sharply at 9.2% in October 2022 before easing back to around 1.5% by late 2024.

Using a conservative long-run average of 2.5% per year, here is what happens to €100,000 left in cash — in terms of what it can actually buy:

Real purchasing power remaining

10 years

~€78,000

20 years

~€61,000

30 years

~€48,000

This is what the long-term 'safe' outcome of cash can deliver to you and your financial wellbeing.

No crash. No scandal. No drama. Just the quiet, steady erosion of what your money is actually worth, at the hands of actual inflation statistics.

For someone retiring at 60 and planning to live well into their 80s, a 2 or 3 decade time horizon, that is not a minor inconvenience, it is a serious retirement income and legacy planning problem.

Yes, Every Advisor in Ireland Will Tell You This Story

Walk into almost any financial advisor's office in Ireland and within about ten minutes, they will show you a version of this inflation chart, the cash mountain, the purchasing power graph. The slow erosion. And then they may slide an investment product across the table!! Inflation's impact on your deposits is a wonderful sales-aid for advisors.

But, and this is important, that doesn't make it wrong!

The fact that a story is used to sell something doesn't make the story untrue. The inflation data is real. The purchasing power erosion is real. The €172 billion sitting in overnight accounts earning close to nothing is real. The case for moving long-term wealth out of cash and into a properly structured investment is sound, provided the investor's attitude and timeframe is appropriate. It just needs to be delivered with honesty rather than fear.

The key question is not whether to invest (assuming you have the risk appetite and time horizon for it). It's how, and with whom.

The Numbers That Actually Matter

There is a lot going on in the world at the moment. There is a war going on. There is fear and loss of life.

From an investment perspective, that creates investor fear and hesitation and worry. Understandably.

However, if you had invested €100,000 into a broadly diversified global equity fund 10, 20, or 30 years ago, with annual fees of around 1%, which is entirely achievable, you would have done very well indeed. Not every year. Not in a straight line, as these things are not linear. But over time, the direction of travel is clear.

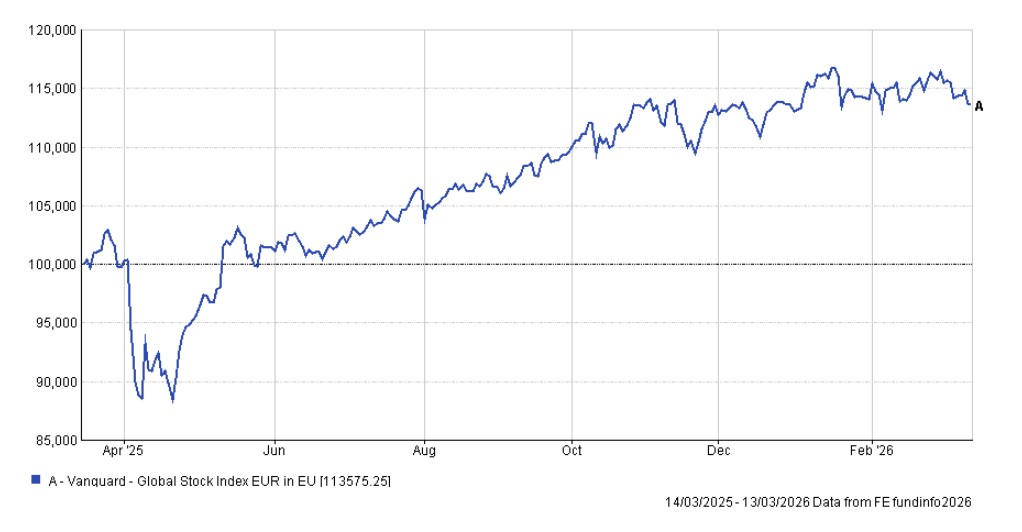

Taking a simple, low-cost and proven Global Equity Fund from vanguard, where one simply invested and stayed invested, up to mid-March 2026;

20 years: €100k = €481k. Annual average return 8%

10 years: €100k = €303k. Annual average return 11.7%

1 year: €100k = €113k. Annual return 11%

As you can see from that 1 year graph, as an example, we had the famous 'Liberation Day' declines in April 2025, followed by sustained growth.

If you were to read the headlines and not look at your account values in the past few weeks, you'd assume that your account is in another downward spiral - but if it is invested similar to the above approach, it certainly isn't.

Don't let fear dictate your investment strategy, nor your fondness for cash!

How much cash are Irish households keeping in low-interest accounts?

Irish households currently hold around €172 billion on deposit, with approximately 85% sitting in overnight or demand accounts earning close to nothing. This is well above the euro-area average and represents a significant long-term cost to savers in lost purchasing power.

Over the past 100 years, the nominal return of mainstream global equities has been around 10% annually, with a real return after inflation of approximately 7%.

We've had to endure years of minus c50% in that time, but patience has been rewarded!

Even after a 1% annual charge, you are still looking at returns that meaningfully outpace inflation over a decade, two decades, or more!

The author and advisor to advisors Nick Murray has spent 50 years distilling this into plain language. His message is consistent and marvellously concise:

"The real long-term risk of equities is not owning them." — Nick Murray, Simple Wealth, Inevitable Wealth

The true risk is not volatility, it's that your money won't grow enough to outpace inflation throughout your life, and you will run out of money.

Not owning equities, Murray argues, is fatal to long-term wealth.

And on the long-term direction of markets: "If you think the market's 'too high' — wait 'til you see it 20 years from now."

This is my personal favourite because it has always been correct!

The advances in equity markets are permanent. The declines are temporary. That investment principle, which is accurate over every meaningful stretch of financial history, is the foundation of long-term investing. It's what we live by.

So What's the Real Risk Here?

Murray argues that relying solely on "safe" fixed-income or cash assets is actually fatal to long-term wealth. This is because the real risk is not short-term volatility, but a permanent loss of purchasing power (as delivered by cash!).

And here is the practical reality I encourage us all to reflect on and apply;

- We don't need a perfect investment

- We don't need to pick the best fund manager in the world

- We need a sensibly diversified, globally spread portfolio, managed with reasonable fees, held patiently over time.

That's it. That's the plan that has always delivered the outcomes most of us seek!

If it's even half-way invested properly, with a fee of around 1%, genuine global diversification, and the discipline to stay invested, history strongly suggests you would have beaten inflation over 10years, beaten it more convincingly over 20, and left it well behind over 30.

Inflation is the real risk. Not the market.

A Final Word.......and a Happy St. Patrick's Day 🍀

Happy St. Patrick's Day, we celebrate everything Irish and green; the fields, the flag, the rivers 😊, and (I'd argue) the long-term upward curve of a well-diversified portfolio. It’s ever-green!

Míse, and the team at Informed Decisions Financial Planning wish you and your family a wonderful St. Patrick's Day. Whether you're at a parade, a match, a pub, a hospital, or quietly ignoring it all over a cup of tea, we hope the day brings you nothing but joy.

And if you've been sitting on a large cash balance wondering whether it's still the right call, maybe this St. Patrick's Day is as good a time as any to start the conversation with someone you trust.

I hope this helps.

Paddy Delaney QFA RPA APA

Disclaimer

The content of this site including blogs and podcasts is for information purposes only. Everybody’s financial situation is different and the content we share on our site and through podcasts may not be applicable to you.

The articles, blogs and podcasts are not investment advice. They do not take account of your individual circumstances, including your knowledge and experience and attitude to risk. Informed Decisions can’t be held responsible for the consequences if you pursue a course of action based on the information we share

Is investing in equities really better than keeping money in cash long term?

Historically, yes. A broadly diversified global equity portfolio, held patiently with annual fees of around 1%, has comfortably outpaced inflation over 10, 20 and 30-year periods. Cash feels safe but loses real value every year. Inflation — not market volatility — is the real long-term risk to your wealth.

You may also like...

July 6, 2026

Sequence of Returns Risk in Ireland: Why the First Decade of Retirement Decides Everything

find out moreRetired or close to it?

Informed Decisions are one of Ireland’s only remaining independent financial advice firms. We specialise in retirement & investment planning for successful individuals, so that our clients only have to retire once.

Find out how we can help...

.svg)