share

Ready for Your Retirement?

Informed Decisions are one of Ireland’s only remaining independent financial advice firms. We specialise in retirement & investment planning for successful individuals, so that our clients only have to retire once.

Retire successfully with Informed Decisions.

informed decisions blog

What Happens to Your Pension When You Change Jobs in Ireland?

June 1, 2026

What are my options if I leave a job and have a pension in Ireland?

You generally have four options: leave the pension where it is as a deferred member, transfer it to your new employer's scheme, transfer it to a Personal Retirement Bond (Buy-Out Bond), or transfer it to a PRSA. Each carries different trade-offs around control, charges, fund options, and lump sum entitlements.

... and the four decisions most Irish professionals get wrong

“Have I lost track of one of my pensions somewhere along the way?”

That's a question that quietly surfaces in conversations with senior professionals more often than it should. Not always in those words. Sometimes it's a subtler version: “I had something with that company I left in 2014, should probably check on that someday.”

In Ireland, the typical professional career involves three or four employers before retirement. Each of those employers may have set up a pension arrangement on the person's behalf. The contributions went in. The fund grew. And then, when the person moved on, the pension didn't always move with them. It stayed where it was,. sometimes consolidated later, sometimes left in default investment mandates, sometimes simply forgotten.

The result is what I'd call the forgotten pension problem. Across a 25-year career, it's not unusual for a senior professional to have €100,000 to €500,000 spread across multiple dormant pensions, often invested conservatively because the original scheme automatically lifestyled them, sometimes facing higher charges than newer arrangements would attract. The money is still there. It just isn't necessarily working as hard as it could.

This article walks through what actually happens to your pension when you change jobs in Ireland: the four decisions you face, what survives a transfer and what doesn't, and the two structural changes from 2026 that have shifted the picture meaningfully. As always: figures and rules reflect the position as at May 2026 and are subject to change. Always verify current rules at revenue.ie and the Pensions Authority, and take independent advice for your specific situation.

The Forgotten Pension Problem: Why Most Irish Professionals Have One

When you contribute to an occupational pension during your time with an employer, the pension is held in trust on your behalf. When you leave that employer, your relationship with the pension changes — but the money doesn't disappear. It becomes either a “preserved benefit” if you've completed at least two years of qualifying service, or a refund of your own contributions if you've left earlier than that.

Two years is the maximum vesting period prescribed by Irish law for occupational pension schemes. If you leave with less than two years' service, you get back your personal contributions (typically less tax already claimed). If you leave with two or more years, the full benefit accrued — including the employer contributions — is preserved in your name as a deferred member of the scheme.

That preservation is helpful. But “preserved” doesn't mean “actively managed”. A deferred pension typically continues to be invested in whatever fund mandate was in place when you left — frequently a default fund, frequently lifestyled, frequently not optimised for someone with another twenty to thirty years of investment runway. And without an active employer relationship, no one is reviewing it on your behalf.

Across multiple jobs, this compounds. The pension from the job you left in 2014 may have been entirely sound at the time — but a decade on, in a default fund that's been gradually de-risked against a target retirement date that no longer reflects your plans, it may not be doing what you'd want it to do.

The forgotten pension problem isn't a problem of carelessness. It's a structural feature of how pensions are administered when employment ends. Solving it starts with knowing what you have.

The Four Decisions When You Leave a Job

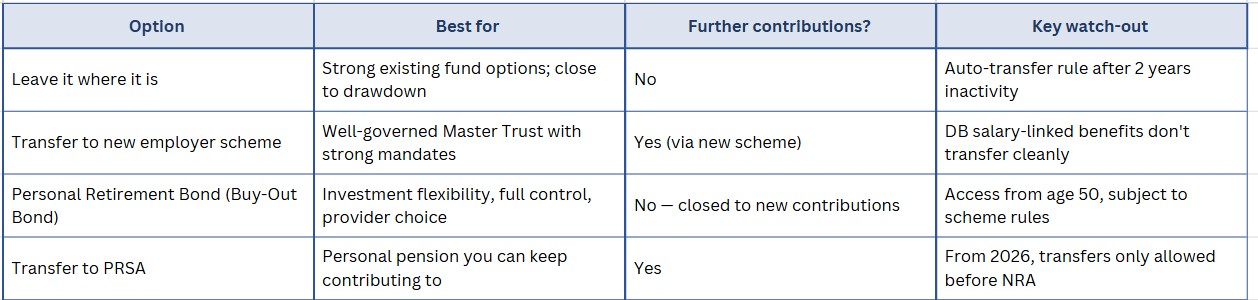

When you leave an employer with a pension, you generally have four options. Knowing which fits your situation requires understanding the trade-offs. The table below summarises the four routes; each is then explored in more detail.

1. Leave it where it is

If you have at least two years' qualifying service, you become a deferred member of the old scheme. The pension stays where it is. The trustees continue to administer it. The investment mandate continues as set. You receive periodic statements but make no further contributions.

This suits you if the existing scheme has strong fund options and reasonable charges, and you don't want the administrative burden of moving it. Also potentially if you're close to drawing benefits — there's less time for any change to compound advantageously.

The watch-out: the auto-transfer rule. If you've been inactive in a scheme for more than two years and made no arrangement, the trustees can transfer your benefits to a Personal Retirement Bond on your behalf — with at least two months' notice. This isn't necessarily bad, but it isn't a decision you should leave to others by default.

2. Transfer to your new employer's pension scheme

If your new employer's scheme accepts incoming transfers, you can move the value of your old pension into the new arrangement. The benefits become part of the new scheme and are administered together going forward.

This suits you if the new scheme has good fund options, the administration is competent, and consolidating reduces the overhead of tracking multiple pots. Particularly attractive when the new scheme is a well-governed Master Trust with strong investment mandates.

The watch-out: salary-and-service-based benefits in defined benefit schemes don't transfer cleanly. If your old pension was a final-salary DB arrangement, transferring out converts it to a money-purchase value — and the salary linkage is lost. For most newer occupational pensions this isn't a concern (they're already DC), but for older schemes or executive arrangements, it matters.

3. Transfer to a Personal Retirement Bond (Buy-Out Bond)

A Personal Retirement Bond, sometimes called a Buy-Out Bond, is an individual pension contract set up in your own name to receive a transfer from a former occupational scheme. Once set up, it's no longer tied to any employer. You choose the provider, you choose the fund mandate, you keep full control.

This suits you if you want investment flexibility and provider choice without remaining linked to a former employer's administration. Particularly useful for senior professionals who want to optimise the investment mandate that was set on autopilot during the employment period.

The watch-out: PRBs don't accept further contributions. Once funded, the bond is closed to new money. So if you anticipate wanting to make additional contributions later, this isn't the right structure for those amounts. Access to a PRB is from age 50, subject to scheme rules.

4. Transfer to a PRSA

Following the Finance Act 2022 reforms, PRSAs can now accept transfers from occupational schemes regardless of length of service. Before 2022, this was restricted to members with under fifteen years' pensionable service — that restriction has been removed. PRSAs are now a viable consolidation vehicle for almost any pension transfer.

This suits you if you want a personal pension you can continue contributing to, with portability across future employments. Particularly powerful when combined with the post-2023 employer-PRSA-contribution rules, which have made employer-funded PRSAs significantly more attractive. The structural side of this question is explored in more detail in our companion analysis of PRSA versus company pension for Irish business owners.

The watch-out: access rules differ from PRBs. PRSAs are generally accessible from age 50 for PAYE employees and age 60 for the self-employed. The 25 % tax-free lump sum applies, subject to the lifetime €200,000 limit aggregated across all benefit crystallisation events.

What is a Personal Retirement Bond in Ireland?

A Personal Retirement Bond — also called a Buy-Out Bond — is an individual pension set up in your own name to receive a transfer from a former occupational pension scheme. It is no longer tied to any employer; you choose the provider and fund mandate. PRBs do not accept further contributions and are accessible from age 50.

What's New in 2026: Two Important Changes

Two structural changes have meaningfully shifted the pension transfer landscape this year. Both are worth knowing about, even if the practical implications for any one individual depend on circumstances.

Auto-enrolment “My Future Fund”, live since 1 January 2026

Ireland's long-promised auto-enrolment scheme launched on 1 January 2026, administered by the new National Automatic Enrolment Retirement Savings Authority (NAERSA). Workers aged between 23 and 60 earning more than €20,000 per year, who are not already members of a workplace pension, are now automatically enrolled.

In year one, contributions are 1.5 % of salary from the employee, matched 1.5 % from the employer, with the State adding a top-up of 33 % of the employee contribution. Contributions scale up over a decade, reaching 6 % / 6 % / 2 % by year ten.

For high earners, the direct impact is usually limited, most are already members of an existing workplace pension and are therefore not auto-enrolled. But the indirect effects matter: junior employees and new hires now have AE arrangements that need coordinating with any other pension setup; HR processes have changed; and when you change jobs, the AE landscape may now be part of the picture in ways it wasn't before. If you're moving to or from a smaller employer, expect AE to be in the conversation.

New restriction: transfers only before Normal Retirement Age

A change taking effect in 2026 means transfers from a group occupational scheme to a personal pension structure (PRSA or PRB) are now only permitted before the member's Normal Retirement Age. After NRA, transfers are largely blocked, since benefits become payable at NRA in most schemes.

For senior professionals approaching late-career exits — particularly those whose Normal Retirement Age in their scheme is 60 or 62 rather than 65 — this is a planning point. If a transfer is part of your retirement structure, it needs to happen before you cross NRA, not after. We've covered the broader context of these changes in our analysis of the major pension updates affecting Irish savers in 2026.

What Survives a Transfer and What Doesn't

When a pension transfers from one structure to another, certain elements move with it intact and certain elements don't. The most common misunderstandings show up here.

What transfers cleanly:

- The capital value of the fund (less any transfer charges or exit fees)

- Time-on-the-clock for tax-relieved status - the contributions remain pension assets

- The lifetime aggregate counted toward the Standard Fund Threshold

What doesn't transfer cleanly:

- Salary-and-service-linked benefits in defined benefit schemes. Transferring out of a final-salary scheme converts your benefit to a money-purchase value, and the salary linkage is lost.

- The 1.5× salary lump sum entitlement that some occupational schemes offer with twenty or more years of service. PRSAs and PRBs apply the standard 25 %-of-fund lump sum rule. For long-service directors, this can be a meaningful difference.

- Specific death-in-service benefits linked to the employment. These are typically replaced with the standard ARF / PRB inheritance treatment, which works differently.

- Investment mandate continuity. The new structure starts with whatever default the new provider applies - usually requiring an active mandate review to align with your time horizon.

The lifetime €200,000 tax-free lump sum limit is aggregated across all benefit crystallisation events, across all your pension arrangements over your lifetime. Consolidating multiple pensions doesn't change the aggregate limit, but it can affect the timing of when the lump sum is drawn.

Considerations for High-Net-Worth Individuals

For senior professionals approaching retirement with significant accumulated assets, several specific issues require attention.

Standard Fund Threshold proximity. The SFT is €2.2m in 2026, rising in stages to €2.8m by 2029. Pension benefits aggregate across all your arrangements, so consolidating four or five pensions into a single value can bring you closer to the threshold than you may have realised. For HNW individuals, modelling the trajectory before consolidating is part of the planning conversation.

Director and executive pension exits. If you're a business owner or director leaving your own company, through a sale, succession, or transition, the executive pension is rarely a simple consolidation problem. The structural choices interact with the company exit, the timing of any tax-free lump sum, retirement relief on the business sale, and the ongoing investment mandate.

Multi-pot management. Consolidation isn't always the right answer. Splitting benefits across multiple PRSAs or PRBs can support phased drawdown — accessing different pots at different times to manage tax bands and income flexibility. Whether to consolidate or split depends on your retirement timeline, expected income structure, and tax position.

The auto-transfer trap. As mentioned earlier, trustees can transfer dormant occupational scheme benefits to a PRB after two years of inactivity, with two months' notice. This isn't necessarily a problem — but it isn't a decision you should leave to others. Reviewing dormant pensions before that two-year window matters.

Coordination with tax relief planning. Where you sit on the age-related contribution table interacts with how you structure your active and deferred pensions. If you're maximising current contributions, the structure receiving those contributions matters. We've explored this side of the question in our analysis of pension tax relief in Ireland.

The Annual Pension Audit

The single most actionable habit for solving the forgotten pension problem is a yearly review. It doesn't need to be complicated. Three questions, run once a year, capture most of the value.

1. Where are all my pensions, and what is each one worth?

A simple list: provider, fund value, current investment mandate, retirement date assumed. Most senior professionals don't have this list written down anywhere; making one is the foundation of any consolidation or review decision.

2. Is each one invested for the time horizon I actually have?

A pension that was set up at 35 with a target retirement age of 65 may have been lifestyled into bonds and cash years ago, even though your actual retirement plan now is 70 and you have twenty or more years of investment runway. Reviewing each fund mandate matters.

3. Are the structures still right — and is consolidation worth doing?

Sometimes yes, sometimes no. The trade-offs depend on charges, fund options, lump sum rules, and your overall retirement structure. The point isn't to consolidate by default — it's to make the decision deliberately.

This review fits naturally with the year-end pension contribution review. Done together, the contribution decision and the structure decision form a coordinated annual picture.

Final Thoughts

When you change jobs in Ireland, your pension doesn't follow automatically. The decision about what happens to it is yours, and the four options each carry different consequences. Most senior professionals end up with multiple pensions over a career, and the most consistent finding in client conversations is the same: people don't know what they have, where it is, or whether it's working.

The 2026 changes: auto-enrolment going live, and the new pre-NRA restriction on group-scheme transfers — make this a particularly relevant year to run the audit. So does the broader regulatory backdrop: Standard Fund Threshold rising to €2.8m by 2029, PRSA reforms still bedding in, the IORP II transition just completed.

Three actions, taken every twelve months, capture most of the available benefit. First, list every pension you have: provider, value, fund mandate, intended retirement date. Second, review each fund mandate against your actual time horizon. Third, decide deliberately whether to leave each one where it is, transfer it, or consolidate, rather than letting the decision happen by inertia.

The cost of leaving the forgotten pension problem unsolved doesn't show up as a fine. It shows up as a quieter retirement than the one you've actually built the assets for.

I hope this helps.

Paddy Delaney QFA RPA APA

Disclaimer

The content of this site including blogs and podcasts is for information purposes only. Everybody’s financial situation is different and the content we share on our site and through podcasts may not be applicable to you.

The articles, blogs and podcasts are not investment advice. They do not take account of your individual circumstances, including your knowledge and experience and attitude to risk. Informed Decisions can’t be held responsible for the consequences if you pursue a course of action based on the information we share

Do I lose my pension if I leave my job after one year in Ireland?

The maximum vesting period under Irish law is two years. If you leave with less than two years' qualifying service, you typically receive a refund of your own contributions only — the employer contributions are not preserved. With two or more years, your full benefit becomes preserved in the scheme as a deferred member.

You may also like...

July 6, 2026

Sequence of Returns Risk in Ireland: Why the First Decade of Retirement Decides Everything

find out more

Retired or close to it?

Informed Decisions are one of Ireland’s only remaining independent financial advice firms. We specialise in retirement & investment planning for successful individuals, so that our clients only have to retire once.

Find out how we can help...

.svg)