share

Ready for Your Retirement?

Informed Decisions are one of Ireland’s only remaining independent financial advice firms. We specialise in retirement & investment planning for successful individuals, so that our clients only have to retire once.

Retire successfully with Informed Decisions.

informed decisions blog

Financial Advisor Commissions in Ireland: What Are You Actually Paying?

March 23, 2026

What is the difference between initial and trail commission on an Irish ARF or pension?

Initial commission is a once-off payment to the broker when a product is arranged — typically a percentage of the lump sum invested. Trail commission is an ongoing annual payment from your fund for as long as the policy exists. On a €1 million ARF, 5.25% initial equals €52,500 upfront, while 1% trail equals €10,000 every year thereafter.

There's a document that every regulated financial intermediary in Ireland is legally required to publish, if they receive any commission income. It's called a Remuneration Summary and it sets out, in plain terms, every commission, fee, and form of payment that firm can receive from the product provider whose products it recommends and sells to you.

It is a template, at least until the actual fee section, that starts with the following wording:

The background

Pursuant to provision 4.58A of the Central Bank of Ireland's September 2019 Addendum

to the Consumer Protection Code, all intermediaries, must make available in their

public offices, or on their website if they have one, a summary of the details of all

arrangements for any fee, commission, other reward or remuneration provided to the

intermediary which it has agreed with its product producers.

The issue is that most people have never read one of these things!

That's not entirely surprising. These documents tend to live quietly in the footer of a broker's website, written in language dense enough to discourage casual reading. But if you're approaching retirement with a significant pension pot, and you've never actually looked at your advisor's charges document, there's a reasonable chance you don't and won't understand or realise what you're paying, or for how long.

We recently reviewed the publicly available charges document of one Irish intermediary firm, lets call them Nudge n Wink Limited, trading as Caveat Emptor FInancial. A friend of Informed Decisions Financial Planning asked us to review their offering and their approach, which we did for them.

To be clear, Caveat Emptor Financial are complying with the rules; they've published this document as required under provision 4.58A of the Central Bank of Ireland's Consumer Protection Code. They are not unusual. Their commission structures are broadly representative of what is available to commission-based brokerages across the Irish market. It is one of the things that makes financial advice firms so attractive to aggregators; as you'll ready about on a monthly basis in the papers these days.

Which is precisely why the numbers are worth talking about.

What the Document Actually Shows

Caveat Emptor's charges document covers multiple product providers and product types. For those of you approaching or in retirement, the figures that matter most are those relating to pensions, ARFs, and investments. Here is what is disclosed.

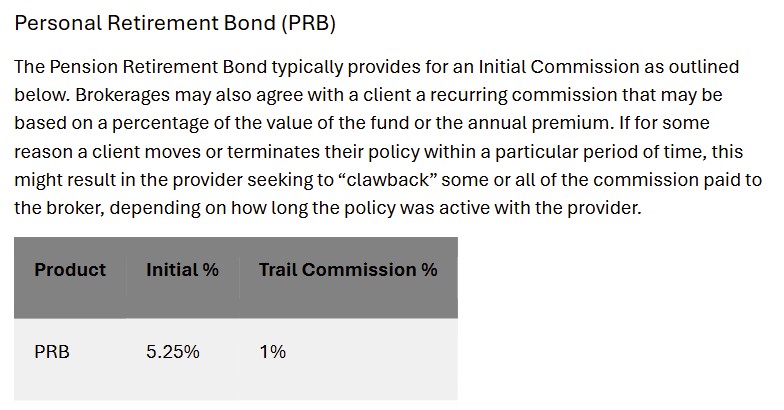

For a single premium pension (a lump sum into a pension), the maximum initial commission available is 5.25% with a trail commission of 1% per annum. For an Approved Retirement Fund (ARF), the product many of you will be moving into at retirement, the maximum initial commission is also 5.25%, with a trail commission of 1% per annum. For a Personal Retirement Bond (PRB), often used when transferring a pension from a previous employer, the initial commission runs to 5.25% and trail to 1%.

For regular premium pensions, the initial commission available rises to 20% of the first year's contributions, with trail of 1% per annum thereafter.

For a Personal Retirement Bond or PRB (also known as Buy out Bond), the document states the below:

These are the maximum figures allowed via the insurance companies on whose behalf they sell pension, investment and protection products to their own clients. The document notes that actual commission charged will depend on individual circumstances and will be disclosed to each client. Nevertheless, these are the numbers the firm confirms are available to them with their product providers. They represent real ceilings that real clients could be paying.

Putting It in Euros

Percentages on paper can feel abstract. In euros, they look rather different.

Say you've just retired and you're moving €500,000 into an ARF through a commission-based broker such as Caveat Emptor Financial, who charge you the maximum initial commission of 5.25%. That's €26,250 leaving your fund on day one (and into their bank account) before your money has had a single hour in the market. On top of that, a trail commission of 1% per annum means €5,000 in year one, and an amount that fluctuates with your fund value each year thereafter, for as long as you hold the product with them.

Over a 20-year retirement on a €500,000 ARF, the trail commission alone, ignoring the compounding effect of the money being removed from your fund, could amount to €80,000 to €100,000 or more, depending on how the fund performs. When you factor in the growth you're not getting on the money being deducted each year, the cumulative drag is considerably higher. We've done the numbers on this kind of long-term fee impact before, and the effect is sobering, particularly if you are not aware of the costs, and are not getting value for money.

If you want to explore that further, our piece (Blog 121) on the long-term impact of fees on your ARF and pension puts real figures on what the drag can look like over a retirement.

A €1 million ARF at the same rates would see €52,500 leave the fund at outset, followed by €10,000 per year in trail. The numbers scale quickly.

But Surely It's Disclosed?

This is the argument most often made in defence of the current system, and it's not entirely wrong. Caveat Emptor's document does disclose these figures. Under the CPC rules, it had to. And the document itself states that commission will be disclosed to each client on a case-by-case basis before any product is arranged.

But there is a meaningful difference between information being available and information being genuinely transparent.

When you sign up for a pension or ARF product, you don't receive a Key Information Document along with your policy schedule. Because there is no obligation on brokers or product providers to do so! However, if you are investing in an investment product, you are obliged to receive a Key Investor Document. Riddle me that!

Whether you get a KID or not, you typically do not receive a clear statement that says: "We will be paid €26,250 from your fund today, and then €5,000 per year for the life of this policy."

Instead, those costs are embedded, folded into the plan charges, the allocation rate, the annual management charge, and reflected in the unit value of your policy statement! The broker's commission becomes indistinguishable from the product's own fees and running costs. You'd need to know exactly what to ask, and to ask it confidently, to have a remote chance of uncovering it.

We've been making this point for years. The greengrocer analogy still holds. If your local shop was taking a cut from the supplier every time it recommended a particular product, and you were paying a quietly inflated price without knowing it, you'd want to know. Financial services is no different. You can read more of our thinking on the structural problem with commissions in our piece on the war on commissions and what it really means for Irish investors.

Are Irish financial advisors required to disclose what commission they earn?

Yes. Under the Central Bank of Ireland's Consumer Protection Code, brokers must publicly disclose the commissions they can receive from product providers, and must disclose these to clients before arranging any product. In practice, however, these figures are often shown as percentages rather than euro amounts, making the real cost easy to overlook.

The Structural Conflict Nobody Names

There is something else worth naming plainly. A system in which an advisor is paid more for recommending higher-value products, or for recommending products with embedded commissions over lower-cost alternatives, creates a structural conflict of interest. Not necessarily a deliberate or malicious one, but a structural one all the same.

An advisor who can earn 5.25% upfront on an ARF product, plus 1% in annual trail, has a very different financial incentive to one who charges a flat annual fee for their time. The first earns more the larger the product recommended and the longer the client stays. The second earns more by doing better work and serving more clients well.

That distinction matters enormously when you have €1 million or more in pension assets. It matters when you are weighing up drawdown strategies, deciding how to structure your ARF income, thinking about how to minimise the tax your estate will face, or considering whether to phase retirement or take benefits early. These are decisions where the difference between genuinely independent advice and structurally incentivised advice can be worth far more than most people realise.

It's all about a Fiduciary Duty, which we operate to; doing what is best for the clients, not just what is deemed 'suitable' - as is the norm in Irish financial advice.

Without trying to blow our own horns here; we did an Informed Decisions MasterPlan with new clients about 18months ago. During that planning project it becase clear, that even allowing for disaster, this couple could comfortably cease working the 60 hour weeks they were doing, cease putting money into pensions and investments. They had enough.

We showed them that how and why this was the case. We encouraged them to instead retire, live a very comfortable life with secure inflation-adusted and tax efficient retirement incomes, while also supporting their adult children in the way that they wished to. Delighted to say that they have since sold their business, aligned their retirement and investment assets with their plans, and are living the dream of travelling, hobbies, family and exercise.

They recently shared with me that had we not worked together, they would still be under the advice of their former advisor, who sole recommendation was that they keep working and keep sending piles of cash into their pensions every month! One can see why that was the advice given! But that conflicted advice cost them a few years of retirement, and would potentially have cost them lots more had we not got to work together.

The question of who exactly the advisor is working for in a commission-based model is one we've explored before in our piece on the changing landscape for independent financial advice in Ireland. It's a question that deserves a straight answer.

What Good Transparency Would Actually Look Like

We're not suggesting that commission-based advisors are all acting against their clients' interests. Many genuinely work hard, keep abreast of the rules, and do right by the people they serve. The issue, as we've said, is the structure and opacity.

Good transparency would mean that before any product is arranged, a client receives a document showing, in euros, not percentages, exactly what the advisor will earn today, and exactly what they will earn each year going forward. It would mean those figures sit prominently in the engagement letter, not buried in a general charges document on a website. It would mean a client can look at those numbers, compare them to what they may already be paying or what others are offering, assess the value for money, and make a fully informed decision about whether the arrangement makes sense or not.

Some firms and product providers seem to do this reasonably well. Many do not.

We're certainly not perfect ourselves but we try to be as upfront and transparent as is possible to be, so we made the decision years ago to publish and promote the fee-only nature of our services, and what it costs! The transparency we show, in my experience only enhances the trust and relationships we have with the people who we get to work with, which is a really nice place to be, as they say!

If you're currently working with a financial advisor or broker and you've never had that conversation, it is absolutely within your rights to ask for it. Ask what initial commission was received on your products, or will be received if assessing a new product, in euros.

Ask what trail commission is being deducted from your fund annually for the brokers, again, in euros.

If you're at the stage of deciding who to work with in the first place, we've put together a practical breakdown of how to find truly independent financial advice in Ireland, including the questions worth asking before you engage anyone. It's worth a read before committing to any arrangement or new product via any broker, whether they state they are fee-only, fee-based, commission-based or some such variation!!

You've worked hard to build what you have. The decisions you make in the years around retirement are among the most consequential financial decisions of your life. You deserve to make them with complete clarity about what your advice is really costing you.

I hope this helps.

Paddy Delaney QFA RPA APA

Disclaimer

The content of this site including blogs and podcasts is for information purposes only. Everybody’s financial situation is different and the content we share on our site and through podcasts may not be applicable to you.

The articles, blogs and podcasts are not investment advice. They do not take account of your individual circumstances, including your knowledge and experience and attitude to risk. Informed Decisions can’t be held responsible for the consequences if you pursue a course of action based on the information we share

What is a fiduciary duty and do Irish financial advisors have one?

A fiduciary duty means an advisor is legally and ethically required to act in your best interests — not simply to recommend something that is deemed "suitable." Most Irish financial advisors operate to a suitability standard, not a fiduciary one. Fee-only, truly independent advisors who operate to a fiduciary standard are rare in Ireland, but they do exist.

You may also like...

August 3, 2026

Zombie Funds: What Nobody Tells You About Private Credit and Equity in Ireland

find out more

Retired or close to it?

Informed Decisions are one of Ireland’s only remaining independent financial advice firms. We specialise in retirement & investment planning for successful individuals, so that our clients only have to retire once.

Find out how we can help...

.svg)